Implementation of the Digital Euro

August 30, 2023 | von: innovate-banking

Veröffentliche eine Notiz:

EXECUTIVE SUMMARY

The digital euro will enter the highly competitive, multifaceted, and heterogeneous payments landscape in the Eurozone. As any other payments method, it needs to provide additional value for the variety of stakeholders to achieve the envisioned acceptance rate in daily payments. Therefore we see the following aspects as levers for a successful digital euro:

Build on existing rails and provide enhancements for the digital euro

We think that the initial acceptance of the digital euro will be very much determined by simplicity and similarity in usage and operations with other well established payment methods, besides commercial models, costs and innovations. Hence, there should be aspiration to benefit from existing rails and standards but provide enhancements where needed, including uniformity across the Eurozone. This is also referenced by the European Commission’s legislative proposal [2]. This would help to avoid slow adoption rates, unnecessary new technical specifications, and expensive implementations. For the long-term success, foundations for innovations need to be built, particularly for strong privacy, uniform digital payments including support for virtual worlds and tokenized economies.

Extend PSD2(3) with a standard digital euro API for incumbents, FinTechs, TPPs

A key element for the acceptance of the digital euro will be the active support by the intermediary landscape, which in itself is very heterogeneous. It ranges from FinTechs, mainly building their business models on sharp value proposition with a strong focus on innovation, to traditional incumbents with an established and rich product set for retail clients and businesses, based on solid systems for payments capture and execution. The digital euro components should integrate very well with the incumbents’ existing infrastructures to support fast adoption rates. We propose to utilize the PSD2(3) role model to its full extent, including third party provider (TPP) roles. Subsequently, the digital euro would benefit from solutions which are already in the market and would enable new solutions built within the same regulatory framework. Extending PSD2(3) with a digital euro specific standard interface, for instance with strong privacy for low-value proximity payments, would enable new innovations. Such an extension could build on quantum-safe encryptions and utilize existing technical rails. Enabling this path would provide a more direct way for the ECB to provide advanced retail payment features as enablers for intermediaries. Of course, this requires a clear governance to not compete with the private sector.

Allow strong privacy for low-value proximity payments, independent of technical connectivity

Strong privacy should be a key differentiator of the digital euro. The legislative proposal of the European Commission [2] already includes strong privacy for offline payments. We think this can also be provided for payments where payer and/or payee are online, assuming that proximity and the payment amount are the determining factors to allow strong privacy and suit anti-financial crime requirements. By allowing strong privacy for a significantly larger volume of cash-like payment transactions a higher adoption rate is very likely, and it would allow for immediate detection of a potential double spend and counterfeiting.

Include a centrally governed distributed ledger as an enabler for digital processes, virtual worlds and tokenized economies

The selection of technologies for the digital euro components is of major importance. A high focus needs to be on non-functional aspects, like strong privacy and security, quantum-safe encryption, resiliency and scalability. The digital euro, in particular the settlement component, needs to address interoperability with the traditional world, but equally important with digital processes and virtual worlds as well as with tokenized economies. This requires a selection of technologies, which are mature and able to serve as a strong foundation for innovations in the next years. We believe that distributed ledger technologies (DLTs) address these needs the best, combined with zero-knowledge proofs to achieve strong privacy. The deployment of the digital euro system should be distributed, but governance can be centralized and hence is in line with European Commission’s and ECB’s objectives. IBM’s implementations demonstrate that high performance and scalability requirements could be reached with such a DLT implementation. Future requirements to provide interoperability for cross-currency payments with other retail CBDCs add to the importance of DLT.

Build the digital euro system by starting with a minimum viable digital euro within a sandbox

Building the digital euro system has many complexity drivers, for instance: large number of users in the Eurozone countries with cultural differences, large existing intermediary landscape, integration of a new payments method with existing heterogeneous IT landscapes, preparation for the next-gen payments infrastructure across Europe, security and business resilience, privacy, and relevant regulations and legal frameworks in general. Systems with such a high complexity are best built with incremental and agile approaches. Built-in end-to-end learning cycles are key for their implementation, including IT and governance.

The first productive version is then usually best built as a minimum viable product (MVP), in this case the minimum viable digital euro. A go-live will then include only minimal but differentiating functionality in order to get early learnings from actual build and production experiences. But such an approach requires that all stakeholders accept and advocate limitations. Finally, a minimum viable digital euro could be launched within a sandbox, where for instance the number of countries and transaction volumes are significantly limited. Users can be restricted to family & friends which could, as an example, translate into individuals employed in financial services. Following the first go-live, releases could be rolled-out in 6-months intervals to gradually augment functionality, add supported countries, user groups and increase transaction volumes as examples.

BUILD ON EXISTING RAILS AND STANDARDS

Since the digital euro is a new form of money, its market adoption is a challenge, which has to be tackled with on several front lines. Encompassing all such fronts is regulation which will have to be updated and amended, if only to explicitly include digital euro in their respective realm. Digital euro as legal tender and a required harmonization of legal tender across Europe will be setting the ground. A clearly defined path to mandatory acceptance, including the scope of acceptance and realistic transition timelines should be set out from the start of the digital euro realisation. The roles and levels of intermediaries should be based on those defined by PSD2, to be extended by stronger, more explicit standards based e.g. on the Berlin GROUP work. Baseline regulation such as GDPR and NIS2 will apply, while other regimes like MiCA need to be analysed for alignment and compatibility. The current legislative proposal of the European Commission [2] is addressing most of these aspects. The further process should add clarity and highlight required downstream consequences.

One essential front line for market adoption includes the digital euro payment instruments created by intermediaries and their implementation. This is an area for competition, ideally fostering innovation and novel instruments for the benefits of the consumers. The ECB model for the digital euro defines a clear role and responsibilities for intermediaries who will have to implement the relevant automated near real time processing and integrate it with their customer front end channels, or possibly create new channels. The new legislative notion of “no channel” or supporting a generic app or somebody else’s channel is a deep intervention which will require detailed standards and their continuous evolution. Enabling the reuse of existing “rails”, implementation patterns and payment messages will be a key success factor for fast and broad technical acceptance. ISO 20022 should be the foundation, included in scheme rule book and implementation guide level documentation and governance as established since the introduction of SEPA.

Special care needs to be taken to preserve competitive choices for clients. It can be debated if full vertical disintermediation is the most promising path, given its complexity. Very detailed technical standards will be required to enable such client choices in practice. A prime example are payment initiation messages from client to bank to start a digital euro payment. Each bank or group of banks could create their own proprietary message, or the digital euro rule book will prescribe a common standard format that every single intermediary will have to support. To state the obvious, this format will need to be an ISO 20022 pain.001 message, highly similar to a pain.001 used to initiate a SEPA Instant payment today. The same holds true for request to pay flows which could rely on SEPA request to pay standards. For payee-initiated payments card industry messages need to be supported. A fully defined common standard will require continuous governance and work so as to keep up with evolving demand and technological advancement.

The same principles apply when going beyond the digital euro payment transaction: balance information or confirmations for payment execution should best be offered in the same ISO camt format that is used for account-based payment transactions. This will make sure that existing cash management solution can easily integrate digital euro as a new form of liquidity. While these services are client-facing and offered by intermediaries it would still be valuable to extend the standardization this far, integrating the governing bodies of interbank standards such as the European Payments Council. As laid out in the European Commission’s legislative proposal [2], the same POS terminal initiating a card payment today should be able to initiate a digital euro payment tomorrow. Same holds true for other established initiation channels, transaction reporting and the likes. Consequently, close alignment with the governing bodies with these standards is desirable, to anchor the digital euro in the existing world rather than a focus on creating a generic app and entirely new detailed “must-do” interface for each and everybody in the payments business.

INTERMEDIARY LANDSCAPE

The Eurozone’s payment landscape provides an already comprehensive set of payment methods, mainly offered by credit institutions, payment service and third-party providers. It is very competitive, innovative, and fast changing. Hence, there must be a clear value proposition towards retail clients, but also towards intermediaries, to achieve the necessary acceptance of the digital euro. This needs to be strongly backed with intrinsic motivation in the market and supported by regulation.

Value for people

It seems that fundamentally two different areas are of primary interest for people in the Eurozone and their retail payments: the digital euro easily integrates with existing payment rails and could be used as an additional alternative payment method. But it needs to come with additional features, comparable or lower costs, and simplicity of usage. Current discussions show that the added value and the uniqueness of the digital euro is very hard to articulate. However, if the digital euro would enable and drive new payment solutions to fill white spots, a clear and novel value could be articulated towards people in the Eurozone. Currently, the following cash-like features of a digital euro seem to be particularly relevant for them:

- Stronger privacy in digital retail payments (person-to-business, person-to-person)

- Strongest privacy in proximity payments, same as with cash (person-to-business, person-to-person)

- Offline payments

We think that cash-like features, like stronger privacy, for person-to-business digital payments, are very important to implement digital inclusion, i.e. payments in digital processes and virtual worlds. In the Eurozone, potential financial instabilities and crises situations are currently not at the forefront in people’s perception – at least not for the larger population. Hence, related capabilities and stability features of the digital euro are not people’s priority.

However, conditional and cross-border payments seem of significantly higher interest. There is also a high interest by non-Eurozone central banks to support cross-border payments in their retail CBDC initiatives. According to the current digital euro planning, these features might come at a later point in time. Nevertheless, technologies to implement the digital euro have to be selected now, and in our opinion, they should already lay the foundations for these functionalities. This includes interoperability and atomic settlement options for digital experiences. Deciding on the usage of DLT is a key technological decision for the digital euro.

Value for intermediaries

For intermediaries there are basically three different categories of value propositions related to the digital euro:

- New business models. The digital euro should enable new profitable business models. Besides typical data monetization driven and commission-based models as we have them today, we would expect additional business models, like strong privacy for a service charge, enhanced integrations with digital processes and virtual world experiences in the future.

- Niche-plays. Utilize the digital euro to implement niche solutions which supplement current offerings by the private sector. Such niche-plays usually address a very limited group of retail clients and are not available today for a reason. Generally, they are not profitable enough to justify necessary investments. Usually in the Eurozone, these plays either fall into the category of financial inclusion and hence could be the primary objective of the ECB, or they would require different underlying payment rails (technology and regulations) to become an attractive target for entrepreneurs. The digital euro could provide such a foundation.

- Minimalistic implementation. Integrate the digital euro into existing payment rails (like cards, SCT Inst, PSD2(3)) with similar features. This is not necessarily leading to new business opportunities, but provides a low-cost option to implement the digital euro according to proposed requirements as a legal tender.

Innovations and new rails

With the digital euro there could be a much more direct way for the ECB and governance bodies to introduce enablers for retail payments more effectively into the market. Once implemented in the digital euro components, they could be immediately utilized by intermediaries. Hence, it would be a direct lever for innovation.

In order to create compelling enablement for a variety of digital processes, the right technologies need to be selected. They should support the straightforward and cost-effective integration with existing payment rails to limit necessary investments for a broader acceptance. But they should also enable entirely new rails and innovations. Tokenization of central bank money is one important area to foster enhancements and new digital processes.

This ambition would mandate that governance bodies are continuously managing the digital euro implementation to maintain it as attractive and up to date for an innovative ecosystem and FinTechs in particular. Efficient governance is essential to keep pace with developments in digital money and stablecoins.

Multi-level intermediary landscape

We see a need for a more granular ecosystem of intermediaries. The future intermediary landscape for the digital euro should be envisioned as multi-level. Planning for more than one intermediary between the retail user and ECB’s digital euro components would better support smaller intermediaries:

- to create very focused innovative offerings, e.g. wallet solutions

- to utilize new and existing payment infrastructure services built by larger providers

- to lower entry barriers

Enabling such a multi-level intermediary landscape would require adequate support by regulations to implement an appropriate license model for more granular services with clear responsibilities. With PSD2(3) and open banking models, foundations are already available.

Options for stronger privacy

The intermediary landscape already implemented GDPR and consent mechanisms to protect people’s privacy. People who prefer for instance the benefits of a single trusted intermediary providing 360-degree views of their financial information could build on existing services augmented by digital euro services and accounts.

With the digital euro options for stronger privacy and self-control could be added. People demanding higher levels of privacy should be able to use separate wallet providers, payment service providers and a credit institution managing the reference account.

Standard APIs within the intermediary landscape

In our opinion standard APIs need to be introduced within the intermediary landscape to enable smaller intermediaries to provide innovative services for retail clients and to indirectly access the digital euro infrastructure. Standard APIs simplify integrations and enable competition.

With PSD2(3), open banking initiatives, SCT Inst and the corresponding European Commission’s legislative proposal (October 2022), there are already enablers in the market to significantly support implementation, rollout and acceptance of the digital euro. But they need to be enhanced and augmented to address digital capabilities of the future and enhanced privacy needs. For instance, PSD2 as it is today, would only support the integration of digital euro payments with existing intermediary payment infrastructures. Stronger privacy for online payments is not addressed.

The positioning of PSD2 in the intermediary architecture landscape is from our point of view also crucial for the digital euro to reach a high acceptance by utilizing the entire PSD2-based ecosystem. Next to PSD2 an extension should be defined to address specifics of the digital euro, particularly enhanced privacy (depicted as D€ PSP API in the picture below). This would enable new, digital euro specific services, implemented as a new path in the intermediary landscape and directly rely on the digital euro components (shown on the left side of the picture).

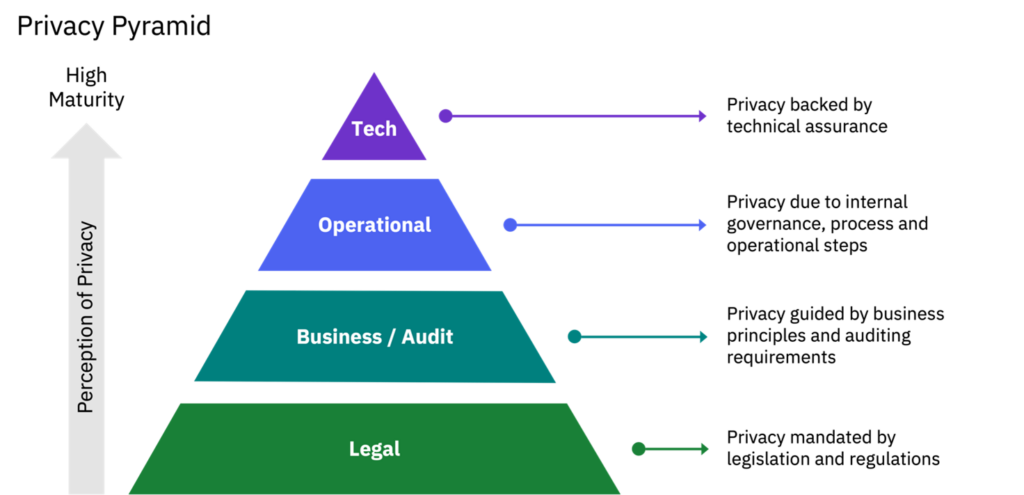

PRIVACY

Multiple surveys and consultations have determined privacy as an essential feature for the successful adoption of the digital euro. Fully anonymizing payments would oppose AML and CFT regulations. Often knowledge of comprehensive payment usage patterns is required to effectively combat illicit activities. The digital euro legislative proposal foresees cash-like privacy for offline payment transactions, while online payment transactions would be consistent with current digital payment’s privacy levels. Consequently, the overall privacy for payers and payees depends on legal, business, operational, and technical protections that are built-in as part of the solution.

Levels of privacy

The legal, business, auditing and operational protections of privacy form the foundation of the privacy solution. The technology layer however can provide the most reliable and robust maturity level of privacy due to its technical assurance.

The digital euro regulatory framework needs to harmonize with several regulations and rulebooks including PSD2(3), SEPA Instant Credit transfer (SCT Inst), SEPA Request-to-Pay (SRTP), GDPR, MiCAR, and KRITIS. From a privacy point of view, a separate category should be created for digital euro payment transactions below a certain pre-set threshold which could be exempted from existing requirements on auditing and record keeping. This ensures higher privacy protections are technically built-in for such transactions.

Strong privacy guidelines and requirements mentioned as part of rulebook and digital euro system requirements would be core to the business layer. In various publications, the ECB has clearly stated that it would not like to have access to information related to end users of the digital euro. Auditing function requirements often mandate availability of transaction information to the regulator. Thus, the roles of dispute and fraud management, and auditors must be designed to ensure the information of end users collected during the payment is retained only to meet legal and regulatory obligations.

A potential digital euro solution would involve multiple parties such as credit institutions, FinTechs and payment service providers. The operational and governance guidelines on data collection and storage need to ensure end-to-end privacy measures.

Technical layer

Every digital interaction creates digital traces that can be aggregated and used to create a larger picture of an individual. It is important that these traces of digital information are retained in the silos they originate from to prevent aggregation and clustering.

Offline transactions to boost privacy The legislative proposal for the digital euro suggests that offline transactions under a certain threshold mirror the privacy of cash payments. Intermediaries would only have insight to funding and defunding transactions. However, the risk of double spending is eminent in offline transactions increasing fraud exposure. We strongly believe that cash-like privacy should not be bound to offline payments only, but be extended to online payments with close-proximity under a certain threshold. This increases the privacy level in a significantly larger number of payments. Ultimately, proximity and transaction value would determine if transactions are private vis-à-vis the intermediary. All other (online) transactions would provide the same privacy as other private digital means of payment (see Figure 4).

Privacy in the settlement engine

The digital euro settlement engine would need to receive only the details of payer and payee intermediaries. However, the intermediaries would be aware of the end user details as they would need to interface with ECB for the settlement.

The settlement engine would have the minimal context information that would be needed to perform, thus end users would not have to trust the process or system to enforce privacy. Auditors could verify the actual implementation. More information required for conditional payments may have to be stored in an isolated system where users would have the option to monitor and manage their payment conditions.

Additional privacy could be achieved by allowing self-custodial wallets where low-value proximity payments could be private against intermediaries. The system could allow users to transact directly with digital euro settlement components, exchanging money bilaterally without intermediaries in the transaction process.

SETTLEMENT WITH DLT

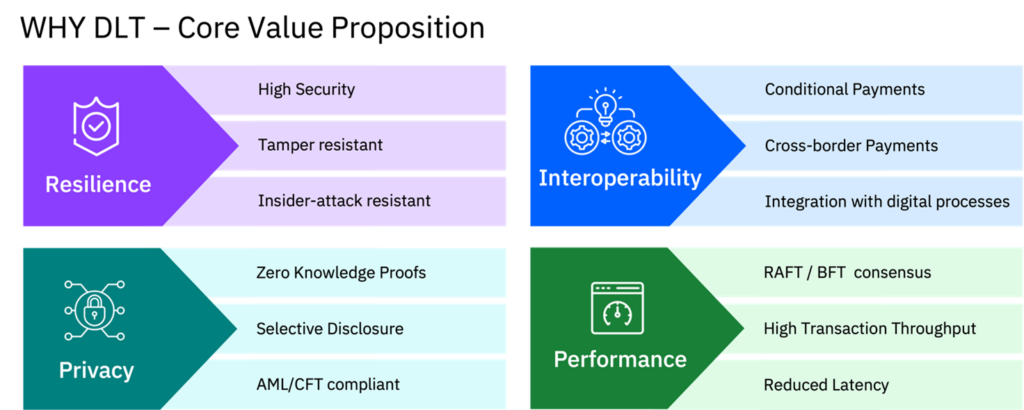

In multiple publications the ECB has expressed the cruciality of sufficient resilience, adaptation of privacy-preserving techniques, interoperability with existing systems, enablement of conditional payments and central governance for oversight, rule establishment, and risk mitigation of the digital euro system. Considering those together with the European Commission’s proposal for a regulation on the establishment of the digital euro [2], and concerns expressed in surveys and market research for such implementations, a solution incorporating DLT best accommodates the needs of the digital euro.

Since the term DLT often gets confused with traditional decentralized blockchain technologies, we want to clarify what degree of distribution we endorse for the digital euro settlement. We strongly recommend a centrally governed distributed ledger that combines the strengths of both centralized and distributed systems. In this type of system, a central entity preserves control over the ledger which is distributed and maintained as per consensus algorithm defined in the system. The term distributed refers to replication of the ledger, for instance across various Eurozone countries.

All in all, DLT is not requisite to build the digital euro system today. However, considering the needs for resilience, privacy, innovation, and interoperability, DLT poses significant advantages for the digital age of payments. The European Commission argues towards that direction by stating that “the digital euro settlement infrastructure should seek to ensure adaptation to new technologies, including distributed ledger technology” ([2], p32).

Resilience

In essence, DLT enhances resilience against system errors, system outages and cyber-attacks by an order of magnitude. Thus, offering significant advantages over conventional systems. By leveraging a consensus process among geographically distant nodes to capture and resolve anomalies, errors through compromised access control or device upgradation errors are dealt with systematically. This eliminates the need for manual reconciliation, enhancing the system’s efficiency and reducing vulnerabilities, since nodes continuously communicate and agree on what transactions follow next. Thus, eliminating the potential of introducing harmful or untruthful transactions to the system. Ultimately, the consensus in the core settlement engine will prevent errors pro-actively.

Furthermore, a DLT incorporating solution can resist device defects, power outages and natural disasters since the integrity of a system is not limited to a few geographical locations but rather distributed to various locations. Accordingly, availability requirements are fulfilled by DLT.

In addition, tamper-resistant and quantum-safe consensus mechanisms safeguard the integrity and validity of data in digital euro settlement, making it highly resistant against tampering, physical attacks and manipulation. Due to DLTs append-only nature, transactions are final and immutable, preventing attacks on past transactions.

But with cyber-criminality on the rise, a system must also be secure against insider attacks. Difficulties arise when systems have to deal with malicious infiltrators. To bolster security against both outside and inside attacks, distributing data entry and validation through DLT mitigates the risk of insider threats, further enhancing the resilience of the digital euro system.

Consensus algorithms Byzantine fault tolerance (BFT) refers to the ability of a network or system to continue functioning even when some components are faulty or have failed. With a BFT-type consensus, a DLT network would keep functioning or implementing planned actions even if only two-thirds of the nodes are reliable and genuine. BFT consensus also better protects the system against insider attacks when compared with Crash Fault Tolerant (CFT) consensus.

While Crash Fault Tolerant (CFT) based systems are secured against a number of unavailable nodes, Byzantine Fault Tolerant (BFT) based systems provide even higher resilience, withholding up to 33% of malicious nodes.

Ultimately, implementing DLT elements for the digital euro provides significant advantages over centralized conventional systems. We highly recommend a DLT solution using BFT consensus as such a solution will provide the highest possible security and resilience that would be needed for digital euro.

Interoperability

Europeans enjoy a diverse landscape of payment options today. To successfully introduce the digital euro as an additional means of payment, it would need to be interoperable with existing payment rails. The ECB [3] recognizes this and states that “[the Eurosystem] should not miss the opportunities offered by the international dimension […] requiring interoperability”.

Retail CBDC solutions offered by central banks outside of the Eurozone are very likely, and it is important that the digital euro can interoperate with those in cross-border and cross-currency transactions. Scalable interoperability between independent payment systems is required to ensure the relevance of the digital euro.

By employing DLT-based structures, separate retail CBDC infrastructures could be connected via bridges. Solutions like Hyperledger Cacti and Hyperledger Weaver demonstrate the scalable interconnectivity between independent distributed ledgers. Whereas today’s fragmented cross-border payment infrastructure of nostro and vostro accounts bear high transaction fees, tied up liquidity and slow settlement speeds, DLT based systems with common standards allow for instantaneous settlement with feasible fees and just-in-time liquidity accordingly. DLT provides a transformative solution for the digital euro, enabling collaboration and consensus. Interoperability through secure communication channels allows the ECB to coordinate policies and establish common standards fostering regulatory harmonization, reducing fragmentation and ensuring interoperability across jurisdictions. By leveraging DLT capabilities, the ECB can build a trusted and interconnected ecosystem, facilitating efficient collaboration and an interoperable financial landscape.

Moreover, DLT incorporating systems can implement (foundations for) conditional payments, enabling code-based transactions to be executed according to pre-defined conditions, thus facilitating innovative use cases and further automation. Conditional payments are foreseen to be executed on top of the digital euro platform fostering innovation and competition among PSPs. An implementation including DLT elements will provide an infrastructure that supports the provision of complex products and services. The ECB will set out a detailed framework with rules and standards for the development of such. Unlike the basic reservation and release of funds restricting one’s liquidity, this would include novel features like atomic settlement and automated solutions for the industry 4.0. The demand for conditional payments is evident in the growing market value of stablecoins that utilize smart contracts for complex transactions. Eventually, a DLT incorporating solution will position the ECB at the forefront of innovation.

Privacy with DLT

Privacy is the cornerstone of most central banks investigating retail CBDC. The ECB as well emphasizes the importance of privacy and that it will not have access to personal data.

Technologies like zero-knowledge proofs (ZKPs) and blind signatures are employed to preserve personal data. With ZKPs, transaction requests can be processed without revealing any personal data, e.g. validating that a transaction limit for a person has not been exceeded. Accordingly, the level of privacy is adjustable by selectively disclosing data.

Privacy could even be enhanced by allowing self-custodial wallets for the digital euro, as it was already addressed in the ECB’s prototyping phase. For instance, low-value proximity payments could be private against intermediaries since a DLT based settlement allows users to transact directly without the need for intermediaries. By offering users control over their data and transactions, and by using secure payment methods, DLT based wallets increase privacy in digital payment systems significantly.

A DLT’s natural transparency combined with selective disclosure could give auditors the option to validate privacy measures in the settlement engine without obtaining individual’s data.

Throughput and sustainability

Throughput and sustainability issues of cryptocurrencies shed an untruthful light on DLT systems in general. While cryptocurrencies usually struggle to scale their performance, permissioned DLT systems can achieve the necessary transaction throughput to operate a mass payment system. In such a permissioned DLT system all participants could be centrally governed and authenticated. Based on project Hamilton, ECB’s throughput specifications and IBM’s own experiments and validations, we are fully confident that sufficient scalability and throughput can be achieved, even for load profiles in crises stress situations. In several conducted experiments, we found that a sufficient level of throughput can be achieved using either BFT-type or CFT consensus algorithms, though CFT results in higher throughput.

Whereas several cryptocurrencies rely on extensive computing power, not all DLT systems entail a huge carbon emission footprint. In IBM’s own permissioned DLT implementation the computational power requisite to maintain the integrity of the system is comparable to non-DLT systems. Since nodes of permissioned DLTs are generally trusted, the consensus mechanism is optimistic but checks against untruthful commitments to secure the system against outside and inside attacks. Hence, extensive consumption of computing power is avoided.

MINIMUM VIABLE DIGITAL EURO

Building and establishing the system for the digital euro will be a very complex program. As already described in the EXECUTIVE SUMMARY there are many challenges along several dimensions. Effectively managing the implementation risk, including regulatory, governance and IT topics, will be a key success factor.

Approach for implementation

From our experiences, systems with such a high complexity are best built with incremental and agile approaches. As an industry we learned over the last decades that large systems as well as large increments built in a waterfall approach have a high risk to overrun in time and cost. Built-in learning and feedback cycles are key for the implementation of large complex systems.

The first productive version is then usually best approached and built as a minimum viable product (MVP). Literally meaning that the first go-live is with a minimum implementation and rollout. This requires that all stakeholders are committed to the approach and accept limitations in various dimensions. But it is always a hard exercise to achieve consensus on a real minimum between stakeholders.

We think that such a model could also be introduced for the digital euro, where a minimum viable digital euro could be provided after 12 months of implementation and rolled out into production. Then, within reasonable short timeframes enhancements can be delivered and the scope can be broadened gradually. In this case, we think 6-month intervals are reasonable.

Benefits and objectives of a minimum viable digital euro

This approach would provide several key benefits:

- Faster time2market. Various kinds of (international) digital currencies, including stablecoins, which are planned or already launched will be competing with the digital euro as digital payment methods. We think that the digital euro should be launched rather earlier than later – and before private sector digital currencies will reach market dominance.

- Early on validation of acceptance, concepts and technologies. Early understanding and validating acceptance by all stakeholders, including payer and payees, will be key for the general acceptance of the digital euro. Concepts and the envisioned architecture should be validated in terms of practicalities within the entire ecosystem, since basic adjustments are easier before a system reaches its full scale.

- Improved plannability and program risk mitigation. With a minimum viable digital euro the full lifecycle will be executed and learnings, particularly from the ecosystem, can be brought into follow-on releases to improve plannability and risk mitigation.

Constraints

But compared to application development in enterprises, establishing the digital euro is a significantly different environment for applying such an MVP based approach. For instance, consensus and priorities on requirements, timelines as well as regulation and legal definitions require significantly longer lead times. Since the digital euro is an ecosystem play, change and side effects on credit institutions and payment service providers need to be understood. For example, validating and stabilizing APIs early on in an MVP is key. This helps to avoid cascading effects in the intermediary landscape when the system reached already full scale.

Preparations for a minimum viable digital euro

A suitable approach requires preparations of course. For the digital euro the complex environment has to be addressed properly. Since the minimum viable digital euro lays the foundation and will be productive, foundations in terms of architecture, technology decisions as well as governance and operations need to be clear on a high-level, so that the implementation work can be started. As a concrete example, end-to-end scenarios, including the intermediary landscape, need to be sufficiently clear as a pre-requisite. As soon as a minimum viable digital euro enters production, of course the legal and regulatory framework needs to be in place.

Focus of the minimum viable digital euro

We propose to start with a very focused and minimalistic set of functionalities and restrict the minimum viable digital euro in several dimensions. We recommend to focus on the biggest concerns of users as payers and payees with the very first release. Our thoughts on possible limitations for a minimum viable digital euro are listed in Figure 7.

Download as PDF:

ABOUT THE AUTHORS

Wolfgang Berger

Partner, CTO Banking and Financial Markets (DACH), IBM Consulting

Wolfgang is a very experienced architect and technical lead for large transformation programs in banking and financial markets. He has a broad expertise in digital transformations, platforms, payments, digital assets, and digital currencies.

Thomas Hartmann

Associate Partner, Leader Payments and DLT Banking, IBM Consulting

With 30+ years of experience in payments Thomas has supported transformation and innovation in retail and wholesale, national and global payments. He established DLT based approaches with digital money and assets, focusing on integrating innovation into the existing landscape.

Atakan Kavuklu

Digital Assets Consultant, IBM Consulting

Atakan is specialized in digital money & assets and voluntarily supports the CBDC Tracker and the Digital Euro Association. He has a degree in International Economics and Development.

Naren Krishnan

Lead Digital Assets Architect, IBM Consulting

Naren has led several digital assets solutions including tokenization of securities, Carbon credits and stablecoins. Recently, Naren is involved in the design of wholesale and retail CBDC.

Arindam Dasgupta

Senior Digital Assets Architect, IBM Consulting

Arindam has architected several payment and digital assets solutions including asset tokenization, privacy preserving systems and self-sovereign identity. He has earned the prestigious distinction of receiving double gold medals in academics, holds couple of patents on DLT space and a fellow of Digital Euro Association.

REFERENCES

[1] Proposal for a REGULATION OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL amending Regulations (EU) No 260/2012 and (EU) 2021/1230 as regards instant credit transfers in euro, 26-Oct 2022

[2] Proposal for a REGULATION OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL on the establishment of the digital euro, 28-Jun 2023

[3] Eurogroup, International aspects of CBDCs: update on digital euro, 15-May 2023

© Copyright IBM Corporation 2023

IBM Corporation

1 New Orchard Road

Armonk, NY 10504

IBM, the IBM logo, and ibm.com are trademarks of International Business Machines Corp., registered in many jurisdictions worldwide. Other product and service names might be trademarks of IBM or other companies. A current list of IBM trademarks is available on the Web at “Copyright and trademark information” at www.ibm.com/legal/copytrade.shtml.

This document is current as of the initial date of publication and may be changed by IBM at any time. Not all offerings are available in every country in which IBM operates.

THE INFORMATION IN THIS DOCUMENT IS PROVIDED “AS IS” WITHOUT ANY WARRANTY, EXPRESS OR IMPLIED, INCLUDING WITHOUT ANY WARRANTIES OF MERCHANTABILITY, FITNESS FOR A PARTICULAR PURPOSE AND ANY WARRANTY OR CONDITION OF NONINFRINGEMENT. IBM products are warranted according to the terms and conditions of the agreements under which they are provided.

Leadership Skills in the Digital Transformation Wave of Central Banks

In an era of unprecedented change, many companies are faced with the challenges of digital transformation. Becoming a digital business means using technology to create new value in business models, customer experiences, and the internal capabilities that support core operations, whilst also generating efficiencies. The successful adoption of new technologies, digital ways of working and […]

Warum ein IT Leitstand ohne AI Tools möglich, aber nicht sinnvoll ist

Es gibt Statements unter Hundebesitzern, die fangen etwa so an : „Ein Leben ohne Hund ist zwar möglich, aber nicht erfüllend und daher sinnlos“. Ganz so krass ist die Einstellung in der IT unter Systemadministratoren und Site Reliability Engineers noch nicht, was den Einsatz von Tools angeht. Aber die Sinnhaftigkeit des Einsatzes von AI Algorithmen […]

Implementation of the Digital Euro

EXECUTIVE SUMMARY The digital euro will enter the highly competitive, multifaceted, and heterogeneous payments landscape in the Eurozone. As any other payments method, it needs to provide additional value for the variety of stakeholders to achieve the envisioned acceptance rate in daily payments. Therefore we see the following aspects as levers for a successful digital […]